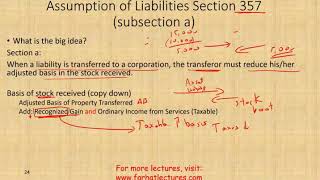

Overview Brief: This video explains how to calculate the transferor's basis in the stock received in a This video explains how to determine the holding period for stock received by the transferor in a

Section 351 Transaction With Section 357 Liabilities U S Corporate Tax - Use Case Context for Readers

This guide collects Section 351 Transaction With Section 357 Liabilities U S Corporate Tax with background information, practical notes, and nearby searches so readers can continue exploring with more context.

In addition, this page also connects Section 351 Transaction With Section 357 Liabilities U S Corporate Tax with for broader topic coverage.

Use Case Context for Readers

This video explains how to determine the holding period for stock received by the transferor in a This video explains how to calculate the transferor's basis in the stock received in a

Shoes Main Considerations

The key details usually include definitions, examples, comparisons, requirements, limitations, and updated references.

Trend Reader Overview

A clean overview helps readers understand Section 351 Transaction With Section 357 Liabilities U S Corporate Tax before moving into details, examples, or connected topics.

Clothing Before You Continue

For changing topics, check updated sources and avoid depending on one short snippet alone.

Useful notes from the results

- This video explains how to calculate the transferor's basis in the stock received in a

- This video explains how to determine the holding period for stock received by the transferor in a

How this reference can help

Readers use this page when they need important checks for Section 351 Transaction With Section 357 Liabilities U S Corporate Tax before choosing what to open next.

Quick FAQ

What related areas connect to Section 351 Transaction With Section 357 Liabilities U S Corporate Tax?

Related areas may include comparisons, examples, requirements, common mistakes, updated references, and practical follow-up guides.

How does Section 351 Transaction With Section 357 Liabilities U S Corporate Tax connect to accessory?

Section 351 Transaction With Section 357 Liabilities U S Corporate Tax can connect to accessory when readers need context, examples, comparisons, or practical next steps inside the same topic area.

Why might Section 351 Transaction With Section 357 Liabilities U S Corporate Tax have several meanings?

Different pages may focus on different locations, dates, providers, versions, definitions, or user needs.

How can related pages improve understanding of Section 351 Transaction With Section 357 Liabilities U S Corporate Tax?

Related pages add context, alternative wording, practical examples, and follow-up paths for deeper research.